Reports

Reports

Analysts’ Viewpoint on Intraosseous Devices Market Scenario

Intraosseous devices or intraosseous infusions can be used to deliver medications and fluids in an emergency situation where venous access is unavailable or cannot be quickly established. Intraosseous devices may help patients receive fluids and treatments through the bone marrow in a safe, effective, and practical manner. The global intraosseous devices market is growing at a steady pace due to the increase in geriatric population, rise in prevalence of various diseases, surge in research activities, rise in number of medical emergency situations, and increase in developmental activities and approaches in the healthcare sector in developed and developing countries. Growth in number of emergency cases, such as heart attacks and trauma-related attacks, is expected to propel the global intraosseous devices market in the next few years.

Medical professionals and trained staff are required to use intraosseous devices as a reliable backup when intravenous access is not possible. Intravenous access in children is challenging and slow. Hence, intraosseous route has emerged as the preferred route in pediatric resuscitation. The device is easily inserted into the medullary space of bone, and the flow of intravenous fluid into the device indicates accurate positioning. Manual needles were the first intraosseous devices to be introduced, which are still extensively used by several practitioners. Several different manual intraosseous needles are commercially available in the market. Recent developments in the intraosseous devices market suggest that manufacturers are investing significantly in research and development activities in order to introduce effective products that increase the efficiency of the therapeutic process. The global intraosseous devices market is driven by improvements in needle tips, new needle assembly, and catheter improvements. Cutting-edge designs and usage of premium materials are also propelling the global intraosseous devices market.

Value-added features offered by intraosseous devices in order to provide effective and efficient vascular access, resulting in positive outcomes and medical aid and care, are expected to drive the global intraosseous device market size in the near future. Intraosseous devices are used to provide effective and quick treatment in different medical situations, particularly emergencies. Medical professionals and trained personnel must use intraosseous devices as an effective alternative when intravenous access is not possible. Companies are strengthening their research & developmental activities and expanding their product lines in order to offer value-added features for the future market demand for intraosseous devices.

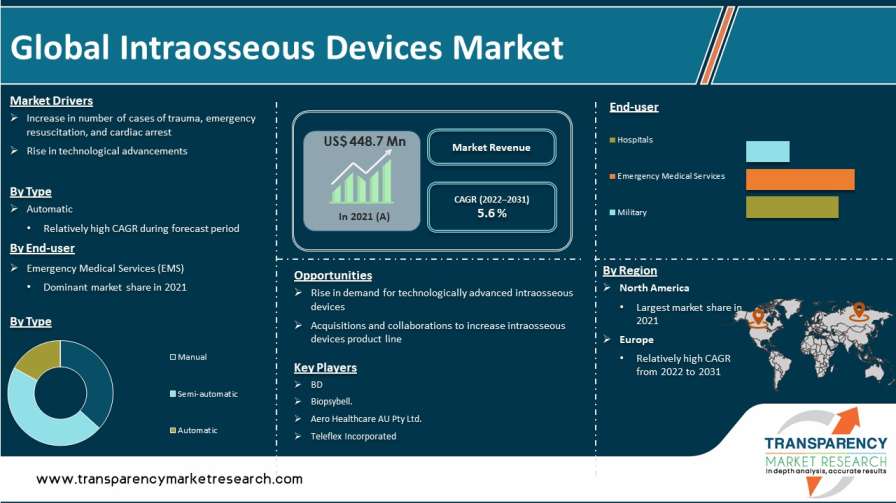

Rise in prevalence of trauma cases, emergency resuscitation, and cardiac arrests has increased the patient pool requiring intraosseous access across the world, resulting in high demand for intraosseous devices. According to Heart Disease and Stroke Statistics - 2017 Update by American Heart Association, more than 350,000 out-of-hospital cardiac arrests (OHCA) are reported in the U.S. annually; around 90% of these result in death. Furthermore, in 2015, the annual incidence of EMS-assessed non-traumatic OHCA stood at around 356,500. Moreover, 7,037 children suffer OHCA each year.

In terms of type, the global intraosseous devices market has been classified into manual, semi-automatic, and automatic. Semi-automatic intraosseous devices are more user-friendly than manual devices, and also provide quicker and easier vascular access. Penetration of semi-automatic devices is higher than automatic intraosseous devices. Semi-automatic intraosseous devices provide a wider range of products as compared to manual and automatic intraosseous devices. Demand for semi-automatic devices has increased owing to the availability of more options in the market.

Based on end-user, the global intraosseous market has been classified into hospitals, emergency medical services, and military. The emergency medical services (EMS) segment held the largest share of the global intraosseous devices market in 2021. The segment is expected to grow at a rapid pace during the forecast period. Rise in number of road accidents, trauma cases, cardiac arrests, and other disorders is projected to increase the number of emergency medical situations. This, in turn, is anticipated to augment the EMS segment. High prevalence of diseases, particularly pediatric diseases, and surge in the patient population undergoing emergency situations lead to an increase in the usage of intraosseous devices to provide emergency medical services (EMS).

North America was a highly attractive market for intraosseous devices in 2021. The market in the region is projected to grow at a high CAGR during the forecast period. Highest incidence and prevalence of emergency medical cases and presence of key players in the U.S. are the major factors propelling the intraosseous devices market in the region.

The intraosseous devices market in Europe is expected to grow at a moderate pace during the forecast period. The market in the region is driven by rise in incidence of medical emergency cases and increase in geriatric population. The European Resuscitation Council (ERC) recommends intraosseous access devices during CPR if peripheral vein access is not immediately available. Intraosseous access is a widely accepted method of gaining venous access during a critically ill child's cardiopulmonary resuscitation (CPR).

The market in Asia Pacific is expected to experience notable growth during the forecast period. Increase in access to health care services through non-profit organizations in collaboration with governments, rapid introduction of advanced technological systems in developing countries, and rise in frequency of emergency medical situations are driving the intraosseous devices market in the region. Growth in prevalence of traffic accidents, trauma cases, and other medical emergencies is propelling the intraosseous devices market in Latin America.

The global intraosseous devices market is fragmented, with the presence of many large-scale players. Key players operating in the global intraosseous devices market are Aero Healthcare AU Pty Ltd., Becton, Dickinson and Company (BD), Biopsybell, Cook, PAVmed, Inc., PERSYS MEDICAL, and Teleflex Incorporated. These players are adopting growth strategies such as new product development, product launches, product approval, agreement, partnerships, and mergers.

Leading players have been profiled in the intraosseous devices market report based on parameters such as company overview, financial overview, business strategies, product portfolio, business segments, and recent developments.

|

Attribute |

Detail |

|

Market Size Value in 2021 |

US$ 448.7 Mn |

|

Market Forecast Value in 2031 |

More than US$ 778.9 Mn |

|

Growth Rate (CAGR) 2022-2031 |

5.6% |

|

Forecast Period |

2022–2031 |

|

Historical Data Available for |

2017–2021 |

|

Quantitative Units |

US$ Mn for Value |

|

Market Analysis |

It includes segment analysis as well as regional level analysis. Moreover, qualitative analysis includes drivers, restraints, opportunities, key trends, Porter’s Five Forces analysis, value chain analysis, and key trend analysis. |

|

Competition Landscape |

|

|

Format |

Electronic (PDF) + Excel |

|

Market Segmentation |

|

|

Regions Covered |

|

|

Countries Covered |

|

|

Companies Profiled |

|

|

Customization Scope |

Available upon request |

|

Pricing |

Available upon request |

The global intraosseous devices market was valued at US$ 448.7 Mn in 2021

The global intraosseous devices market is projected to reach more than US$ 778.9 Mn by 2031

The global intraosseous devices market grew at a CAGR of 6% from 2017 to 2021

The global intraosseous devices market is anticipated to grow at a CAGR of 5.6% from 2022 to 2031

The automatic segment held major share of around 45% of the global intraosseous devices market in 2021

North America is expected to account for major share of the global intraosseous devices market during the forecast period.

Aero Healthcare AU Pty Ltd., Becton, Dickinson and Company, Biopsybell, Cook, and Teleflex Incorporated

1. Preface

1.1. Market Definition and Scope

1.2. Market Segmentation

1.3. Key Research Objectives

1.4. Research Highlights

2. Assumptions and Research Methodology

3. Executive Summary: Global Intraosseous Devices Market

4. Market Overview

4.1. Introduction

4.1.1. Segment Definition

4.2. Overview

4.3. Market Dynamics

4.3.1. Drivers

4.3.2. Restraints

4.3.3. Opportunities

4.4. Global Intraosseous Devices Market Analysis and Forecast, 2017–2031

4.4.1. Market Revenue Projections (US$ Mn)

5. Key Insights

5.1. Technological Advancements

5.2. Regulatory Scenario by Region/globally

5.3. Covid-19 Impact Analysis

6. Global Intraosseous Devices Market Analysis and Forecast, by Type

6.1. Introduction & Definition

6.2. Key Findings / Developments

6.3. Market Value Forecast, by Type, 2017–2031

6.3.1. Manual

6.3.2. Semi-automatic

6.3.3. Automatic

6.4. Market Attractiveness Analysis, by Type

7. Global Intraosseous Devices Market Analysis and Forecast, by End-user

7.1. Introduction & Definition

7.2. Key Findings / Developments

7.3. Market Value Forecast, by End-user, 2017–2031

7.3.1. Hospitals

7.3.2. Emergency Medical Services

7.3.3. Military

7.4. Market Attractiveness Analysis, by End-user

8. Global Intraosseous Devices Market Analysis and Forecast, by Region

8.1. Key Findings

8.2. Market Value Forecast, by Region

8.2.1. North America

8.2.2. Europe

8.2.3. Asia Pacific

8.2.4. Latin America

8.2.5. Middle East & Africa

8.3. Market Attractiveness Analysis, by Region

9. North America Intraosseous Devices Market Analysis and Forecast

9.1. Introduction

9.1.1. Key Findings

9.2. Market Value Forecast, by Type, 2017–2031

9.2.1. Manual

9.2.2. Semi-automatic

9.2.3. Automatic

9.3. Market Value Forecast, by End-user, 2017–2031

9.3.1. Hospitals

9.3.2. Emergency Medical Services

9.3.3. Military

9.4. Market Value Forecast, by Country, 2017–2031

9.4.1. U.S.

9.4.2. Canada

9.5. Market Attractiveness Analysis

9.5.1. By Type

9.5.2. By End-user

9.5.3. By Country

10. Europe Intraosseous Devices Market Analysis and Forecast

10.1. Introduction

10.1.1. Key Findings

10.2. Market Value Forecast, by Type, 2017–2031

10.2.1. Manual

10.2.2. Semi-automatic

10.2.3. Automatic

10.3. Market Value Forecast, by End-user, 2017–2031

10.3.1. Hospitals

10.3.2. Emergency Medical Services

10.3.3. Military

10.4. Market Value Forecast, by Country/Sub-region, 2017–2031

10.4.1. Germany

10.4.2. U.K.

10.4.3. France

10.4.4. Italy

10.4.5. Spain

10.4.6. Rest of Europe

10.5. Market Attractiveness Analysis

10.5.1. By Type

10.5.2. By End-user

10.5.3. By Country/Sub-region

11. Asia Pacific Intraosseous Devices Market Analysis and Forecast

11.1. Introduction

11.1.1. Key Findings

11.2. Market Value Forecast, by Type, 2017–2031

11.2.1. Manual

11.2.2. Semi-automatic

11.2.3. Automatic

11.3. Market Value Forecast, by End-user, 2017–2031

11.3.1. Hospitals

11.3.2. Emergency Medical Services

11.3.3. Military

11.4. Market Value Forecast, by Country/Sub-region, 2017–2031

11.4.1. China

11.4.2. India

11.4.3. Japan

11.4.4. Australia & New Zealand

11.4.5. Rest of Asia Pacific

11.5. Market Attractiveness Analysis

11.5.1. By Type

11.5.2. By End-user

11.5.3. By Country/Sub-region

12. Latin America Intraosseous Devices Market Analysis and Forecast

12.1. Introduction

12.1.1. Key Findings

12.2. Market Value Forecast, by Type, 2017–2031

12.2.1. Manual

12.2.2. Semi-automatic

12.2.3. Automatic

12.3. Market Value Forecast, by End-user, 2017–2031

12.3.1. Hospitals

12.3.2. Emergency Medical Services

12.3.3. Military

12.4. Market Value Forecast, by Country/Sub-region, 2017–2031

12.4.1. Brazil

12.4.2. Mexico

12.4.3. Rest of Latin America

12.5. Market Attractiveness Analysis

12.5.1. By Type

12.5.2. By End-user

12.5.3. By Country/Sub-region

13. Middle East & Africa Intraosseous Devices Market Analysis and Forecast

13.1. Introduction

13.1.1. Key Findings

13.2. Market Value Forecast, by Type, 2017–2031

13.2.1. Manual

13.2.2. Semi-automatic

13.2.3. Automatic

13.3. Market Value Forecast, by End-user, 2017–2031

13.3.1. Hospitals

13.3.2. Emergency Medical Services

13.3.3. Military

13.4. Market Value Forecast, by Country/Sub-region, 2017–2031

13.4.1. GCC

13.4.2. South Africa

13.4.3. Rest of Middle East & Africa

13.5. Market Attractiveness Analysis

13.5.1. By Type

13.5.2. By End-user

13.5.3. By Country/Sub-region

14. Competition Landscape

14.1. Market Player - Competition Matrix (by tier and size of companies)

14.2. Market Share Analysis, by Company, 2021

14.3. Company Profiles

14.3.1. Aero Healthcare AU Pty Ltd.

14.3.1.1. Company Overview

14.3.1.2. Product Portfolio

14.3.1.3. SWOT Analysis

14.3.1.4. Financial Overview

14.3.1.5. Strategic Overview

14.3.2. BD

14.3.2.1. Company Overview

14.3.2.2. Product Portfolio

14.3.2.3. SWOT Analysis

14.3.2.4. Financial Overview

14.3.2.5. Strategic Overview

14.3.3. Biopsybell

14.3.3.1. Company Overview

14.3.3.2. Product Portfolio

14.3.3.3. SWOT Analysis

14.3.3.4. Financial Overview

14.3.3.5. Strategic Overview

14.3.4. Cook

14.3.4.1. Company Overview

14.3.4.2. Product Portfolio

14.3.4.3. SWOT Analysis

14.3.4.4. Financial Overview

14.3.4.5. Strategic Overview

14.3.5. Teleflex Incorporated

14.3.5.1. Company Overview

14.3.5.2. Product Portfolio

14.3.5.3. SWOT Analysis

14.3.5.4. Financial Overview

14.3.5.5. Strategic Overview

14.3.6. PAVmed, Inc.

14.3.6.1. Company Overview

14.3.6.2. Product Portfolio

14.3.6.3. SWOT Analysis

14.3.6.4. Financial Overview

14.3.6.5. Strategic Overview

14.3.7. PERSYS MEDICAL

14.3.7.1. Company Overview

14.3.7.2. Product Portfolio

14.3.7.3. SWOT Analysis

14.3.7.4. Financial Overview

14.3.7.5. Strategic Overview

List of Tables

Table 01: Global Intraosseous Devices Market Size Value (US$ Mn) Forecast, by Type 2017-2031

Table 02: Global Intraosseous Devices Market Size Value (US$ Mn) Forecast, by End-user, 2017-2031

Table 03: Global Intraosseous Devices Market Size Value (US$ Mn) Forecast, by Region, 2017-2031

Table 04: North America Intraosseous Devices Market Size Value (US$ Mn) Forecast, by Country, 2017-2031

Table 05: North America Intraosseous Devices Market Value (US$ Mn) Forecast, by Type, 2017-2031

Table 06: Europe Intraosseous Devices Market Value (US$ Mn) Forecast, by Country/Sub-region, 2017-2031

Table 07: Europe Intraosseous Devices Market Value (US$ Mn) Forecast, by Type, 2017-2031

Table 08: Europe Intraosseous Devices Market Value (US$ Mn) Forecast, by End-user, 2015–2025

Table 09: Asia Pacific Intraosseous Devices Market Value (US$ Mn) Forecast, by Country/Sub-region, 2017-2031

Table 10: Asia Pacific Intraosseous Devices Market Value (US$ Mn) Forecast, by Type, 2017-2031

Table 11: Asia Pacific Intraosseous Devices Market Value (US$ Mn) Forecast, by End-user, 2017-2031

Table 12: Latin America Intraosseous Devices Market Value (US$ Mn) Forecast, by Country/Sub-region, 2017-2031

Table 13: Latin America Intraosseous Devices Market Value (US$ Mn) Forecast, by Type, 2017-2031

Table 14: Latin America Intraosseous Devices Market Value (US$ Mn) Forecast, by End-user, 2017-2031

Table 15: Middle East & Africa Intraosseous Devices Market Value (US$ Mn) Forecast, by Country/Sub-region, 2017-2031

Table 16: Middle East & Africa Intraosseous Devices Market Value (US$ Mn) Forecast, by Type, 2017-2031

Table 17: Middle East & Africa Intraosseous Devices Market Value (US$ Mn) Forecast, by End-user, 2017-2031

List of Figures

Figure 01: Global Intraosseous Devices Market Snapshot

Figure 02: Global Intraosseous Devices Market Size (US$ Mn) Forecast, 2017–2031

Figure 03: Global Intraosseous Devices Market Value Share, by Type (2021)

Figure 04: Global Intraosseous Devices Market Value Share, by End-user (2021)

Figure 05: Global Intraosseous Devices Market Value Share, by Region (2021)

Figure 06: Global Intraosseous Devices Market Value Share (%), by Type, 2017 and 2031

Figure 07: Global Intraosseous Devices Market Revenue (US$ Mn) Forecast and Y-o-Y Growth (%) Projection, by Manual, 2017–2031

Figure 08: Global Intraosseous Devices Market Revenue (US$ Mn) Forecast and Y-o-Y Growth (%) Projection, by Semi-automatic, 2017–2031

Figure 09: Global Intraosseous Devices Market Revenue (US$ Mn) Forecast and Y-o-Y Growth (%) Projection, by Automatic, 2017–2031

Figure 10: Global Intraosseous Devices Market Attractiveness Analysis, by Type, 2022–2031

Figure 11: Global Intraosseous Devices Market Value Share (%), by End-user, 2017 and 2031

Figure 12: Global Intraosseous Devices Market Revenue (US$ Mn) Forecast and Y-o-Y Growth (%) Projection, by Hospitals, 2017–2031

Figure 13: Global Intraosseous Devices Market Revenue (US$ Mn) Forecast and Y-o-Y Growth (%) Projection, by Emergency Medical Services, 2017–2031

Figure 14: Global Intraosseous Devices Market Revenue (US$ Mn) Forecast and Y-o-Y Growth (%) Projection, by Military, 2017–2031

Figure 15: Global Intraosseous Devices Market Attractiveness Analysis, by End-user, 2022–2031

Figure 16: Global Intraosseous Devices Market Scenario, 2021–2031

Figure 17: Global Intraosseous Devices Market Value Share (%), by Region, 2017 and 2031

Figure 18: Global Intraosseous Devices Market Attractiveness Analysis, by Region, 2022–2031

Figure 19: North America Intraosseous Devices Market Revenue (US$ Mn) Forecast and Y-o-Y Growth (%) Projection, 2017–2031

Figure 20: North America Intraosseous Devices Market Attractiveness Analysis, by Country, 2022–2031

Figure 21: North America Intraosseous Devices Market Value Share (%), by Country, 2017 and 2031

Figure 22: North America Intraosseous Devices Market Value (%) Share, by Type, 2017 and 2031

Figure 23: North America Intraosseous Devices Market Attractiveness Analysis, by Type, 2022–2031

Figure 24: North America Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Manual, 2017–2031

Figure 25: North America Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Semi-automatic, 2017–2031

Figure 26: North America Intraosseous Devices Market Revenue (US$ Mn) Forecast and by Automatic, 2017–2031

Figure 27: North America Intraosseous Devices Market Value Share (%), by End-user, 2017 and 2031

Figure 28: North America Market Attractiveness Analysis, by End-user, 2022–2031

Figure 29: North America Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Hospitals, 2021–2031

Figure 30: North America Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Emergency Medical Services (EMS), 2017–2031

Figure 31: North America Intraosseous Devices Market Revenue (US$ Mn) Forecast and by Military, 2017–2031

Figure 32: Europe Intraosseous Devices Market Revenue (US$ Mn) Forecast and Y-o-Y Growth (%) Projection, 2017–2031

Figure 33: Europe Market Attractiveness Analysis, by Country/Sub-region, 2022–2031

Figure 34: Europe Intraosseous Devices Market Value Share (%), by Country/Sub-region, 2017 and 2031

Figure 35: Europe Intraosseous Devices Market Value Share (%), by Type, 2017 and 2031

Figure 36: Europe Intraosseous Devices Market Value Share (%), by End-user, 2017 and 2031

Figure 37: Europe Intraosseous Devices Market Attractiveness Analysis, by Type, 2022–2031

Figure 38: Europe Intraosseous Devices Market Attractiveness Analysis, by End-user, 2022–2031

Figure 39: Europe Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Manual, 2017–2031

Figure 40: Europe Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Semi-automatic, 2017–2031

Figure 41: Europe Intraosseous Devices Market Revenue (US$ Mn) Forecast and by Automatic, 2017–2031

Figure 42: Europe Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Hospitals, 2017–2031

Figure 43: Europe Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Emergency Medical Services (EMS), 207–2031

Figure 44: Europe Intraosseous Devices Market Revenue (US$ Mn) Forecast and by Military, 2017–2031

Figure 45: Asia Pacific Intraosseous Devices Market Revenue (US$ Mn) Forecast and Y-o-Y Growth (%) Projection, 2017–2031

Figure 46: Asia Pacific Intraosseous Devices Market Attractiveness Analysis, by Country/Sub-region, 2022–2031

Figure 47: Asia Pacific Intraosseous Devices Market Value Share (%), by Country/Sub-region, 2017 and 2031

Figure 48: Asia Pacific Intraosseous Devices Market Value Share (%), by Type, 2017 and 2031

Figure 59: Asia Pacific Intraosseous Devices Market Value Share (%), by End-user, 2017 and 2031

Figure 50: Asia Pacific Intraosseous Devices Market Attractiveness Analysis, by Type, 2022–2031

Figure 51: Asia Pacific Intraosseous Devices Market Attractiveness Analysis, by End-user, 2022–2031

Figure 52: Asia Pacific Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Manual, 2017–2031

Figure 53: Asia Pacific Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Semi-automatic, 2017–2031

Figure 54: Asia Pacific Intraosseous Devices Market Revenue (US$ Mn) Forecast and by Automatic, 2017–2031

Figure 55: Asia Pacific Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Hospitals, 2017–2031

Figure 56: Asia Pacific Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Emergency Medical Services (EMS), 2017–2031

Figure 57: Asia Pacific Intraosseous Devices Market Revenue (US$ Mn) Forecast and by Military, 2017–2031

Figure 58: Latin America Intraosseous Devices Market Revenue (US$ Mn) Forecast and Y-o-Y Growth (%) Projection, 2017–2031

Figure 59: Latin America Intraosseous Devices Market Attractiveness Analysis, by Country/Sub-region, 2022–2031

Figure 60: Latin America Intraosseous Devices Market Value Share (%), by Country/Sub-region, 2017 and 2031

Figure 61: Latin America Intraosseous Devices Market Value Share, by Type, 2017 and 2031

Figure 62: Latin America Intraosseous Devices Market Value Share (%), by End-user, 2017 and 2031

Figure 63: Latin America Intraosseous Devices Market Attractiveness Analysis, by Type, 2022–2031

Figure 64: Latin America Intraosseous Devices Market Attractiveness Analysis, by End-user, 2022–2031

Figure 65: Latin America Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Manual, 2017–2031

Figure 66: Latin America Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Semi-automatic, 2017–2031

Figure 67: Latin America Intraosseous Devices Market Revenue (US$ Mn) Forecast and by Automatic, 2017–2031

Figure 68: Latin America Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Hospitals, 2017–2031

Figure 69: Latin America Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Emergency Medical Services (EMS), 2017–2031

Figure 70: Latin America Intraosseous Devices Market Revenue (US$ Mn) Forecast and by Military, 2017–2031

Figure 71: Middle East & Africa Intraosseous Devices Market Size (US$ Mn) Forecast, 2017–2031

Figure 72: Middle East & Africa Intraosseous Devices Market Attractiveness Analysis, by Country/Sub-region, 2022–2031

Figure 73: Middle East & Africa Intraosseous Market Value Share (%), by Country/Sub-region, 2017 and 2031

Figure 74: Middle East & Africa Intraosseous Devices Market Value Share (%), by Type, 2017 and 2031

Figure 75: Middle East & Africa Intraosseous Devices Market Value Share (%), by End-user, 2017 and 2031

Figure 76: Middle East & Africa Intraosseous Devices Market Attractiveness Analysis, by Type, 2022–2031

Figure 77: Middle East & Africa Intraosseous Devices Market Attractiveness Analysis, by End-user, 2022–2031

Figure 78: Middle East & Africa Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Manual, 2017–2031

Figure 79: Middle East & Africa Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Semi-automatic, 2017–2031

Figure 80: Middle East & Africa Intraosseous Devices Market Revenue (US$ Mn) Forecast and by Automatic, 2017–2031

Figure 81: Middle East & Africa Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Hospitals, 2017–2031

Figure 82: Middle East & Africa Intraosseous Devices Market Revenue (US$ Mn) Forecast, by Emergency Medical Services (EMS), 2017–2031

Figure 83: Middle East & Africa Intraosseous Devices Market Revenue (US$ Mn) Forecast and by Military, 2017–2031

Copyright © Transparency Market Research, Inc. All Rights reserved

Trust Online

Intraosseous Devices Market