Reports

Reports

The need to differentiate active and inactive components in drugs has helped in popularising oncology biosimilars. Research analysts can differentiate drugs on the basis of their inactive components, even when the reference component or drugs remains the same. The importance of oncology biosimilars that can have different actions on cancers of various types has helped in reconciling the growth dynamics of the market. The tremendous relevance of biosimilar therapies for cancer has also helped researchers in emphasizing on the importance of oncology biosimilars.

The Food and Drugs Administration (FDA) in the US has been at the forefront of growth within the global oncology biosimilars market. Approval of several biosimilars by the FDA have been helpful for research entities and organizations. Post 2015, FDA has been actively approving oncology biosimilars, a trend that is expected to gather momentum in the times to follow. filgrastim-sndz (Zarxio) and Bevacizumab-awwb (Mvasi) are two important biosimilars that were lately approved by the FDA. It would be interesting to see the impact of increased pace of approvals on market maturity.

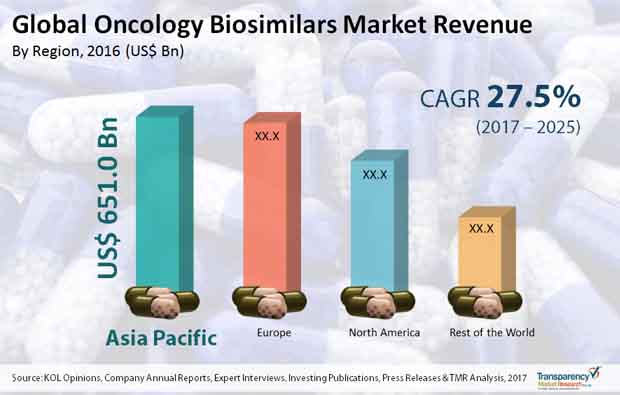

In this preview, several trends, opportunities, and segments pertaining the global oncology biosimilars market have been discussed. The presence of a seamless medical industry that focuses on developing treatment lines for cancer is an important consideration from the standpoint of market analysis. In addition to this, several University scholars have tasted success in developing possible treatment lines for cancer. TMR predicts that the global oncology biosimilars market would grow at a humongous CAGR of 27.5% over the period between 2017 and 2025. The voluminous growth rate can be attributed to investments made in cancer research and analysis. Furthermore, the total worth of the global oncology biosimilars market is set to touch US$17,478.2 mn by 2025-end.

Treatment of Breast Cancer Takes Center Stage Medicine

The global oncology biosimilars market consists of a complex of net of end-uses and applications. Based on disease indication, oncology biosimilars can be segmented into breast cancer, colorectal cancer, neutropenia, lung cancer, and blood cancer. Amongst these, the demand for oncology biosimilars in treating and understanding breast cancer has increased by a dramatic chase. Besides, rising incidence of leukaemia has played to the advantage of the market vendors.

Rising incidence of various types of cancers plays an integral role in driving sales across the global oncology biosimilars market. Clinical research related to oncology has gathered momentum in recent times, and this trend has reflected in the development of several distinct drugs. Research related to leukaemia has especially attracted increased attention from medical researchers. Considering the factors mentioned above, it is safe to predict that the global oncology biosimilars market would gain momentum in the years to follow. Advancements in drug development and analysis of active ingredients in drugs is also an important consideration from the perspective of market growth. Biologic drugs are gradually becoming an important component of the pharmaceutical industry. These drugs are poised to account for a major share of drugs mix produced by the industry.

Regional Dynamics of the Global Oncology Biosimilars Market

On the basis of regions, the global oncology biosimilars market can be segmented into Latin America, North America, Europe, Asia Pacific, and the Middle East and Africa. Investments in cancer research, especially across the UK, are central to the idea of market growth in Europe. Recently, scholars from Cardiff University discovered a potential cure for bodily cancers. The North America oncology biosimilars market is set to expand as new research centers and laboratories emerge in the region.

Some of the leading vendors in the global oncology biosimilars market are Dr. Reddy’s Laboratories Ltd., Intas Pharmaceuticals Ltd., STADA Arzneimittel AG, Pfizer Inc., and Sandoz International GmbH.

Booming Cases of Cancer around the World to Accelerate the Growth Opportunities across the Oncology Biosimilars Market

The oncology biosimilars market is expected to witness a considerable growth-share owing to the rising number of cancer cases across the globe. The increasing number of cancer cases around the world will serve as a vital growth generator for the oncology biosimilars market.

Section 01 Preface

1.1 Market Definition and Scope

1.2 Research Highlights

Section 02 Assumptions and Research Methodology

2.1 Assumptions & Acronyms Used

2.2 Research Methodology

Section 03 Executive Summary: Global Oncology Biosimilars Market

3.1 Executive Summary

3.2 Market Opportunity Map

3.3 Market Overview

3.4 Key Industry Developments

3.5 Global Oncology Biosimilars Market Size (US$ Mn) Forecast, 2015–2025

3.6 Global Oncology Biosimilars Market Outlook

Section 04 Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunity

4.4 Key Trends

Section 05 Porter’s Five Force Analysis

Section 06 Oncology Biosimilars: Key Molecules

Section 07 Biosimilars Market Snapshot

Section 08 Cancer Statistics

Section 09 Global Oncology Biosimilars Market Analysis and Forecasts, By Drug Class

9.1 Introduction & Definition

9.2 Key Findings

9.3 Global Oncology Biosimilars Market Value Share, by Drug Class, 2017 and 2025

9.4 Market Attractiveness By Drug Class

9.5 Global Oncology Biosimilars Market Forecast, by Drug Class, 2015-2025

9.5.1 G-CSF

9.5.2 Monoclonal Antibody

9.5.3 Hematopoietic Agents

9.6 Global Oncology Biosimilars Market Analysis, by Drug Class, 2015-2025

9.7 Key Trends

Section 10 Global Oncology Biosimilars Market Analysis and Forecasts, By Disease Indication

10.1 Introduction & Definition

10.2 Key Findings

10.3 Global Oncology Biosimilars Market Value Share, by Disease Indication, 2017 and 2025

10.4 Market Attractiveness By Disease Indication

10.5 Global Oncology Biosimilars Market Forecast, by Disease Indication, 2015-2025

10.5.1 Breast Cancer

10.5.2 Non-Small Cell lung Cancer

10.5.3 Blood Cancer

10.5.3.1 Leukemia

10.5.3.1.1 Myeloid Leukemia

10.5.3.1.2 Chronic Lymphocytic Leukemia

10.5.3.1.3 Others

10.5.3.2 Non-Hodgkin Lymphoma

10.5.4 Colorectal Cancer

10.5.5 Neutropenia

10.5.6 Others

10.6 Global Oncology Biosimilars Market Analysis, by Disease Indication, 2015-2025

10.7 Key Trends

Section 11 Global Oncology Biosimilars Market Analysis and Forecasts, By Distribution Channel

11.1 Introduction & Definition

11.2 Key Findings

11.3 Global Oncology Biosimilars Market Value Share, by Distribution Channel, 2017 and 2025

11.4 Market Attractiveness By Distribution Channel

11.5 Global Oncology Biosimilars Market Forecast, by Distribution Channel, 2015-2025

11.5.1 Hospital Pharmacy

11.5.2 Online Pharmacy

11.5.3 Retail Pharmacy

11.6 Global Oncology Biosimilars Market Analysis, by Distribution Channel, 2015-2025

11.7 Key Trends

Section 12 Global Oncology Biosimilars Market Analysis and Forecasts, By Region

12.1 Global Market Scenario

12.2 Global Oncology Biosimilars Market Value Share, by Region, 2017 and 2025

12.3 Global Oncology Biosimilars Market Attractiveness, by Region, 2017–2025

12.4 Global Oncology Biosimilars Market Size (US$ Mn) Forecast, by Region, 2015–2025

12.4.1 North America

12.4.2 Europe

12.4.3 Asia Pacific

12.4.4 Rest of the World

Section 13 North America Oncology Biosimilars Market Analysis and Forecast

13.1 North America Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, 2015–2025

13.2 North America Oncology Biosimilars Market Value Share, by Country, 2017 and 2025

13.3 North America Oncology Biosimilars Market Attractiveness, by Country, 2017–2025

13.4 North America Oncology Biosimilars Market Size (US$ Mn) Forecast, by Country, 2015–2025

13.4.1 U.S.

13.4.2 Canada

13.5 North America Oncology Biosimilars Market Value Share, by Drug Class, 2017 and 2025

13.6 North America Oncology Biosimilars Market Attractiveness, by Drug Class, 2017–2025

13.7 North America Oncology Biosimilars Market Size (US$ Mn) Forecast, by Drug Class, 2015–2025

13.7.1 G-CSF

13.7.2 Monoclonal Antibody

13.7.3 Hematopoietic Agents

13.8 North America Oncology Biosimilars Market Value Share, by Disease Indication, 2017 and 2025

13.9 North America Oncology Biosimilars Market Attractiveness, by Disease Indication, 2017–2025

13.10 North America Oncology Biosimilars Market Size (US$ Mn) Forecast, by Disease Indication, 2015–2025

13.10.1 Breast Cancer

13.10.2 Non-Small Cell lung Cancer

13.10.3 Blood Cancer

13.10.3.1 Leukemia

13.10.3.1.1 Myeloid Leukemia

13.10.3.1.2 Chronic Lymphocytic Leukemia

13.10.3.1.3 Others

13.10.3.2 Non-Hodgkin Lymphoma

13.10.4 Colorectal Cancer

13.10.5 Neutropenia

13.10.6 Others

13.11 North America Oncology Biosimilars Market Value Share, by Distribution Channel, 2017 and 2025

13.12 North America Oncology Biosimilars Market Attractiveness, by Distribution Channel, 2017–2025

13.13 North America Oncology Biosimilars Market Size (US$ Mn) Forecast, by Distribution Channel, 2015–2025

13.13.1 Hospital Pharmacy

13.13.2 Online Pharmacy

13.13.3 Retail Pharmacy

13.14 Key Trends

Section 14 Europe Oncology Biosimilars Market Analysis and Forecast

14.1 Europe Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, 2015–2025

14.2 Europe Oncology Biosimilars Market Value Share, by Country, 2017 and 2025

14.3 Europe Oncology Biosimilars Market Attractiveness, by Country, 2017–2025

14.4 Europe Oncology Biosimilars Market Size (US$ Mn) Forecast, by Country, 2015–2025

14.4.1 U.K.

14.4.2 Germany

14.4.3 France

14.4.4 Italy

14.4.5 Russia

14.4.6 Spain

14.4.7 Rest of Europe

14.5 Europe Oncology Biosimilars Market Value Share, by Drug Class, 2017 and 2025

14.6 Europe Oncology Biosimilars Market Attractiveness, by Drug Class, 2017–2025

14.7 Europe Oncology Biosimilars Market Size (US$ Mn) Forecast, by Drug Class, 2015–2025

14.7.1 G-CSF

14.7.2 Monoclonal Antibody

14.7.3 Hematopoietic Agents

14.8 Europe Oncology Biosimilars Market Value Share, by Disease Indication, 2017 and 2025

14.9 Europe Oncology Biosimilars Market Attractiveness, by Disease Indication, 2017–2025

14.10 Europe Oncology Biosimilars Market Size (US$ Mn) Forecast, by Disease Indication, 2015–2025

14.10.1 Breast Cancer

14.10.2 Non-Small Cell lung Cancer

14.10.3 Blood Cancer

14.10.3.1 Leukemia

14.10.3.1.1 Myeloid Leukemia

14.10.3.1.2 Chronic Lymphocytic Leukemia

14.10.3.1.3 Others

14.10.3.2 Non-Hodgkin Lymphoma

14.10.4 Colorectal Cancer

14.10.5 Neutropenia

14.10.6 Others

14.11 Europe Oncology Biosimilars Market Value Share, by Distribution Channel, 2017 and 2025

14.12 Europe Oncology Biosimilars Market Attractiveness, by Distribution Channel, 2017–2025

14.13 Europe Oncology Biosimilars Market Size (US$ Mn) Forecast, by Distribution Channel, 2015–2025

14.13.1 Hospital Pharmacy

14.13.2 Online Pharmacy

14.13.3 Retail Pharmacy

14.14 Key Trends

Section 15 Asia Pacific Oncology Biosimilars Market Analysis and Forecast

15.1 Asia Pacific Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, 2015–2025

15.2 Asia Pacific Oncology Biosimilars Market Value Share, by Country, 2017 and 2025

15.3 Asia Pacific Oncology Biosimilars Market Attractiveness, by Country, 2017–2025

15.4 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast, by Country, 2015–2025

15.4.1 China

15.4.2 India

15.4.3 Japan

15.4.4 Australia & New Zealand

15.4.5 Rest of Asia Pacific

15.5 Asia Pacific Oncology Biosimilars Market Value Share, by Drug Class, 2017 and 2025

15.6 Asia Pacific Oncology Biosimilars Market Attractiveness, by Drug Class, 2017–2025

15.7 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast, by Drug Class, 2015–2025

15.7.1 G-CSF

15.7.2 Monoclonal Antibody

15.7.3 Hematopoietic Agents

15.8 Asia Pacific Oncology Biosimilars Market Value Share, by Disease Indication, 2017 and 2025

15.9 Asia Pacific Oncology Biosimilars Market Attractiveness, by Disease Indication, 2017–2025

15.10 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast, by Disease Indication, 2015–2025

15.10.1 Breast Cancer

15.10.2 Non-Small Cell lung Cancer

15.10.3 Blood Cancer

15.10.3.1 Leukemia

15.10.3.1.1 Myeloid Leukemia

15.10.3.1.2 Chronic Lymphocytic Leukemia

15.10.3.1.3 Others

15.10.3.2 Non-Hodgkin Lymphoma

15.10.4 Colorectal Cancer

15.10.5 Neutropenia

15.10.6 Others

15.11 Asia Pacific Oncology Biosimilars Market Value Share, by Distribution Channel, 2017 and 2025

15.12 Asia Pacific Oncology Biosimilars Market Attractiveness, by Distribution Channel, 2017–2025

15.13 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast, by Distribution Channel, 2015–2025

15.13.1 Hospital Pharmacy

15.13.2 Online Pharmacy

15.13.3 Retail Pharmacy

15.14 Key Trends

Section 16 Rest of the World Oncology Biosimilars Market Analysis and Forecast

16.1 Rest of the World Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, 2015–2025

16.2 Rest of the World Oncology Biosimilars Market Value Share, by Country, 2017 and 2025

16.3 Rest of the World Oncology Biosimilars Market Attractiveness, by Country, 2017–2025

16.4 Rest of the World Oncology Biosimilars Market Size (US$ Mn) Forecast, by Country, 2015–2025

16.4.1 Mexico

16.4.2 Brazil

16.4.3 Rest of the World

16.5 Rest of the World Oncology Biosimilars Market Value Share, by Drug Class, 2017 and 2025

16.6 Rest of the World Oncology Biosimilars Market Attractiveness, by Drug Class, 2017–2025

16.7 Rest of the World Oncology Biosimilars Market Size (US$ Mn) Forecast, by Drug Class, 2015–2025

16.7.1 G-CSF

16.7.2 Monoclonal Antibody

16.7.3 Hematopoietic Agents

16.8 Rest of the World Oncology Biosimilars Market Value Share, by Disease Indication, 2017 and 2025

16.9 Rest of the World Oncology Biosimilars Market Attractiveness, by Disease Indication, 2017–2025

16.10 Rest of the World Oncology Biosimilars Market Size (US$ Mn) Forecast, by Disease Indication, 2015–2025

16.10.1 Breast Cancer

16.10.2 Non-Small Cell lung Cancer

16.10.3 Blood Cancer

16.10.3.1 Leukemia

16.10.3.1.1 Myeloid Leukemia

16.10.3.1.2 Chronic Lymphocytic Leukemia

16.10.3.1.3 Others

16.10.3.2 Non-Hodgkin Lymphoma

16.10.4 Colorectal Cancer

16.10.5 Neutropenia

16.10.6 Others

16.11 Rest of the World Oncology Biosimilars Market Value Share, by Distribution Channel, 2017 and 2025

16.12 Rest of the World Oncology Biosimilars Market Attractiveness, by Distribution Channel, 2017–2025

16.13 Rest of the World Oncology Biosimilars Market Size (US$ Mn) Forecast, by Distribution Channel, 2015–2025

16.13.1 Hospital Pharmacy

16.13.2 Online Pharmacy

16.13.3 Retail Pharmacy

16.14 Key Trends

Section 17 Competition Landscape

17.1 Market Player – Competition Matrix (By Tier and Size of companies)

17.2 Market Share Analysis By Company (2016)

Section 18 Company Profiles

18.1 Sandoz International GmbH

18.1.1 Company Details

18.1.2 Business Overview

18.1.3 Financial Overview

18.1.4 Strategic Overview

18.1.5 SWOT Analysis

18.2 Pfizer, Inc.

18.2.1 Company Details

18.2.2 Business Overview

18.2.3 Financial Overview

18.2.4 Strategic Overview

18.2.5 SWOT Analysis

18.3 Celltrion Inc.

18.3.1 Company Details

18.3.2 Business Overview

18.3.3 Financial Overview

18.3.4 Strategic Overview

18.3.5 SWOT Analysis

18.4 Dr. Reddy’s Laboratories Ltd.

18.4.1 Company Details

18.4.2 Business Overview

18.4.3 Financial Overview

18.4.4 Strategic Overview

18.4.5 SWOT Analysis

18.5 Biocon

18.5.1 Company Details

18.5.2 Business Overview

18.5.3 Financial Overview

18.5.4 Strategic Overview

18.5.5 SWOT Analysis

18.6 Teva Pharmaceutical Industries Ltd.

18.6.1 Company Details

18.6.2 Business Overview

18.6.3 Financial Overview

18.6.4 Strategic Overview

18.6.5 SWOT Analysis

18.7 STADA Arzneimittel AG

18.7.1 Company Details

18.7.2 Business Overview

18.7.3 Financial Overview

18.7.4 Strategic Overview

18.7.5 SWOT Analysis

18.8 Apotex Inc. (Apobiologix)

18.8.1 Company Details

18.8.2 Business Overview

18.8.3 Financial Overview

18.8.4 Strategic Overview

18.8.5 SWOT Analysis

18.9 Intas Pharmaceuticals Ltd.

18.9.1 Company Details

18.9.2 Business Overview

18.9.3 Financial Overview

18.9.4 Strategic Overview

18.9.5 SWOT Analysis

18.10 BIOCAD

18.10.1 Company Details

18.10.2 Business Overview

18.10.3 Financial Overview

18.10.4 Strategic Overview

18.10.5 SWOT Analysis

List of Tables

Table 01 Global Biosimilars Market Snapshot

Table 02 Global Oncology Biosimilars Market Size (US$ Mn) Forecast, by Drug Class, 2015–2025

Table 03 Global Oncology Biosimilars Market Size (US$ Mn) Forecast, by Disease Indication, 2015–2025

Table 04 Global Oncology Biosimilars Market Size (US$ Mn) Forecast, Blood Cancer, 2015–2025

Table 05 Global Oncology Biosimilars Market Size (US$ Mn) Forecast, by Leukemia, 2015–2025

Table 06 Global Oncology Biosimilars Market Size (US$ Mn) Forecast, by Distribution Channel, 2015–2025

Table 07 Global Oncology Biosimilars Market Size (US$ Mn) Forecast, by Region, 2015–2025

Table 08 Approved Oncology Biosimilars by USFDA in new biosimilars pathway established under BPCIA Act

Table 09 North America Oncology Biosimilars: Pipeline Overview, 2017-2020

Table 10 North America Oncology Biosimilars Market Size (US$ Mn) Forecast, by Country, 2015–2025

Table 11 North America Oncology Biosimilars Market Size (US$ Mn) Forecast, by Distribution Channel, 2015–2025

Table 12 Europe Oncology Biosimilars Market Size (US$ Mn) Forecast, by Country, 2015–2025

Table 13 Europe Oncology Biosimilars Market Size (US$ Mn) Forecast, by Drug Class, 2015–2025

Table 14 Europe Oncology Biosimilars Market Size (US$ Mn) Forecast, by Disease Indication, 2015–2025

Table 15 Europe Oncology Biosimilars Market Size (US$ Mn) Forecast, by Blood Cancer, 2015–2025

Table 16 Europe Oncology Biosimilars Market Size (US$ Mn) Forecast, by Leukemia, 2015–2025

Table 17 Europe Oncology Biosimilars Market Size (US$ Mn) Forecast, by Distribution Channel, 2015–2025

Table 18 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast, by Country, 2015–2025

Table 19 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast, by Drug Class, 2015–2025

Table 20 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast, by Disease Indication, 2015–2025

Table 21 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast, by Blood Cancer, 2015–2025

Table 22 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast, by Leukemia, 2015–2025

Table 23 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast, by Distribution Channel, 2015–2025

Table 24 Rest of the World Oncology Biosimilars Market Size (US$ Mn) Forecast, by Country, 2015–2025

Table 25 Rest of the World Oncology Biosimilars Market Size (US$ Mn) Forecast, Drug Class, 2015–2025

Table 26 Rest of the World Oncology Biosimilars Market Size (US$ Mn) Forecast, by Disease Indication, 2015–2025

Table 27 Rest of the World Oncology Biosimilars Market Size (US$ Mn) Forecast, by Blood Cancer, 2015–2025

Table 28 Rest of the World Oncology Biosimilars Market Size (US$ Mn) Forecast, by Leukemia, 2015–2025

Table 29 Rest of the World Oncology Biosimilars Market Size (US$ Mn) Forecast, by Distribution Channel, 2015–2025

List of Figures

Fig. 01 Global Oncology Biosimilars Market Size (US$ Mn) Forecast, 2015–2025

Fig. 02 Global Oncology Biosimilars Market Value Share, by Drug Class (2016)

Fig. 03 Global Oncology Biosimilars Market Value Share, by Disease Indication (2016)

Fig. 04 Global Oncology Biosimilars Market Value Share, by Distribution Channel (2016)

Fig. 05 Global Oncology Biosimilars Market Value Share, by Region (2016)

Fig. 06 U.S. Prevalence Share (%), By Cancer Type, 2015

Fig. 07 Global Estimation of Cancer, By New Cases & Deaths, 2017

Fig. 08 Global Oncology Biosimilars Market Value Share, by Drug Class, 2017 and 2025

Fig. 09 Global Oncology Biosimilars Market Attractiveness, by Drug Class, 2017–2025

Fig. 10 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Monoclonal Antibody, 2015–2025

Fig. 11 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Hematopoietic Agents, 2015–2025

Fig. 12 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by G-CSF, 2015–2025

Fig. 13 Global Oncology Biosimilars Market Value Share, by Disease Indication, 2017 and 2025

Fig. 14 Global Oncology Biosimilars Market Attractiveness, by Disease Indication, 2017–2025

Fig. 15 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Breast Cancer, 2015–2025

Fig. 16 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Non-small Cell Lung Cancer, 2015–2025

Fig. 17 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Blood Cancer, 2015–2025

Fig. 18 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Colorectal Cancer, 2015–2025

Fig. 19 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Neutropenia, 2015–2025

Fig. 20 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Others, 2015–2025

Fig. 21 Global Oncology Biosimilars Market Value Share, by Distribution Channel, 2017 and 2025

Fig. 22 Global Oncology Biosimilars Market Attractiveness, by Distribution Channel, 2017–2025

Fig. 23 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Online Pharmacy, 2015–2025

Fig. 24 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Retail Pharmacy, 2015–2025

Fig. 25 Global Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, by Hospital Pharmacy, 2015–2025

Fig. 26 Global Oncology Biosimilars Market Value Share, by Region, 2017 and 2025

Fig. 27 Global Oncology Biosimilars Market Attractiveness, by Region, 2017–2025

Fig. 28 North America Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, 2015–2025

Fig. 29 North America Oncology Biosimilars Market Value Share, by Country, 2017 and 2025

Fig. 30 North America Oncology Biosimilars Market Attractiveness, by Country, 2017–2025

Fig. 31 North America Oncology Biosimilars Market Value Share, by Distribution Channel, 2017 and 2025

Fig. 32 North America Oncology Biosimilars Market Attractiveness, by Distribution Channel, 2017–2025

Fig. 33 Europe Oncology Biosimilars Market Revenue (US$ Mn) and Y-o-Y Growth (%) Forecast, 2015–2025

Fig. 34 Europe Oncology Biosimilars Market Value Share, by Country, 2017 and 2025

Fig. 35 Europe Oncology Biosimilars Market Attractiveness, by Country, 2017–2025

Fig. 36 Europe Oncology Biosimilars Market Value Share, by Drug Class, 2017 and 2025

Fig. 37 Europe Oncology Biosimilars Market Attractiveness, by Drug Class, 2017–2025

Fig. 38 Europe Oncology Biosimilars Market Value Share, by Disease Indication, 2017 and 2025

Fig. 39 Europe Oncology Biosimilars Market Attractiveness, by Disease Indication, 2017–2025

Fig. 40 Europe Oncology Biosimilars Market Value Share, by Distribution Channel, 2017 and 2025

Fig. 41 Europe Oncology Biosimilars Market Attractiveness, by Distribution Channel, 2017–2025

Fig. 42 Asia Pacific Oncology Biosimilars Market Size (US$ Mn) Forecast and Y-o-Y Growth (%), 2015–2025

Fig. 43 Asia Pacific Oncology Biosimilars Market Value Share, by Country, 2017 and 2025

Fig. 44 Asia Pacific Oncology Biosimilars, Market Attractiveness, by Country, 2017–2025

Fig. 45 Asia Pacific Oncology Biosimilars Market Value Share, by Drug Class, 2017 and 2025

Fig. 46 Asia Pacific Oncology Biosimilars Market Attractiveness, by Drug Class, 2017–2025

Fig. 47 Asia Pacific Oncology Biosimilars Market Value Share, by Disease Indication, 2017 and 2025

Fig. 48 Asia Pacific Oncology Biosimilars Market Attractiveness, by Disease Indication, 2017–2025

Fig. 49 Asia Pacific Oncology Biosimilars Market Value Share, by Distribution Channel, 2017 and 2025

Fig. 50 Asia Pacific Oncology Biosimilars Market Attractiveness, by Distribution Channel, 2017–2025

Fig. 51 Rest of the World Oncology Biosimilars, Market Size (US$ Mn) Forecast and Y-o-Y Growth (%), 2015–2025

Fig. 52 Rest of the World Oncology Biosimilars Market Value Share, by Country, 2017 and 2025

Fig. 53 Rest of the World Oncology Biosimilars, Market Attractiveness, by Country, 2017–2025

Fig. 54 Rest of the World Oncology Biosimilars Market Value Share, by Drug Class, 2017 and 2025

Fig. 55 Rest of the World Oncology Biosimilars Market Attractiveness, by Drug Class, 2017–2025

Fig. 56 Rest of the World Oncology Biosimilars Market Value Share, by Disease Indication, 2017 and 2025

Fig. 57 Rest of the World Oncology Biosimilars Market Attractiveness, by Disease Indication, 2017–2025

Fig. 58 Rest of the World Oncology Biosimilars Market Value Share, by Distribution Channel, 2017 and 2025

Fig. 59 Rest of the World Oncology Biosimilars Market Attractiveness, by Distribution Channel, 2017–2025

Fig. 60 Global Oncology Biosimilars Market Share, by Company, 2016

Fig. 61 Breakdown of Net Sales of Sandoz International GmbH (A Novartis Division), by Franchise, 2016 (%)

Fig. 62 Revenue (US$ Bn) & Y-o-Y Growth (%) of Sandoz International GmbH (A Novartis Division), 2013–2016

Fig. 63 Breakdown of Net Sales of Pfizer, Inc., by Region, 2016 (%)

Fig. 64 Revenue (US$ Bn) & Y-o-Y Growth (%) of Pfizer, Inc., 2013–2016

Fig. 65 Breakdown of Net Sales of Celltrion Inc., by Business Segments , 2016

Fig. 66 Revenue (US$ Mn) & Y-o-Y Growth (%) of Celltrion Inc., 2013–2016

Fig. 67 Breakdown of Net Sales of Dr. Reddy’s Laboratories Ltd., by Business Segments, 2016 (%)

Fig. 68 Revenue (US$ Bn) & Y-o-Y Growth (%) of Dr. Reddy’s Laboratories Ltd., 2013–2016

Fig. 69 Breakdown of Net Sales of Biocon, by Business Segments, 2016 (%)

Fig. 70 Revenue (US$ Mn) & Y-o-Y Growth (%) of Biocon, 2013–2016

Fig. 71 Breakdown of Net Sales of Teva Pharmaceutical Industries Ltd., by Business Segments, 2016 (%)

Fig. 72 Revenue (US$ Bn) & Y-o-Y Growth (%) of Teva Pharmaceutical Industries Ltd., 2013–2016

Fig. 73 Breakdown of Net Sales of STADA Arzneimittel AG, by Business Segments, 2016 (%)

Fig. 74 Revenue (US$ Bn) & Y-o-Y Growth (%) of STADA Arzneimittel AG, 2013–2016

Fig. 75 Revenue (US$ Mn) & Y-o-Y Growth (%) of Intas Pharmaceuticals Ltd., 2013–2016

Copyright © Transparency Market Research, Inc. All Rights reserved

Trust Online

Oncology Biosimilars Market