Reports

Reports

Ambulatory surgery is defined as surgical and diagnostic intervention that does not require overnight hospital stay. The ambulatory surgery has been increasingly adopted by patient population in Europe owing to its safe, high quality, cost-effective and time saving approach to perform surgical interventions. In addition, advancements in technologies that enables healthcare professionals to perform multiple minimally invasive surgical procedures in a single day further drives the market growth in Europe. For example, advent of minimally invasive surgeries such as laparoscopic procedures has permitted complex surgeries such as gallbladder, hysterectomy surgeries to be done in reduced amount of time. However, factors such as lack of adequate medical facilities and favorable reimbursement policies for inpatient surgeries as compared to outpatient surgeries might impede the growth of Europe ambulatory surgical and emergency center services market.

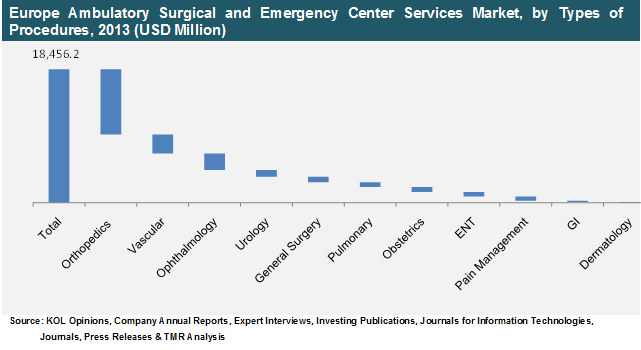

In 2013, the orthopedic surgeries segment accounted for the largest share. Dominance of this market segment was majorly due to high cost of procedures coupled with rising prevalence of arthroscopic procedures. The ophthalmology surgeries segment is expected to grow at the highest growth rate during the forecast period from 2014 to 2020. Factors such as rising number of ophthalmology procedures performed and increasing number of cataract, diabetic retinopathy and other ophthalmology surgeries are supporting the growth of this market segment in the European region. In terms of market volume, ophthalmology segment recorded the highest number of ambulatory procedures and is expected to dominate the market in future. Growing number of ophthalmology procedures that can be done on a daily basis coupled with advancement in ophthalmology ambulatory surgical procedures will help this segment to record high revenue. Moreover, orthopedic surgeries recorded second highest number of ambulatory procedures in 2013. The growth of this segment is due to persistent rise in geriatric population coupled with growing trend of minimally invasive surgeries that helps large number of orthopedic surgeries to be done on ambulatory basis.

U.K. dominated the Europe ambulatory surgical and emergency center services market in 2013. The dominance of this region was mainly attributed to rising government and medical professional bodies’ initiatives to promote ambulatory services in the country. For instance, in November 2014, the British Association of Day Surgery in collaboration with the Healthcare Conferences UK (HCUK) organized an event titled “Improving Quality in Day Surgery”. This event aims at discussing new way to improve quality of day surgery in European countries such as the U.K. and Germany. Rest of the Europe (RoE) accounted for the highest number of ambulatory surgeries performed in 2013 and is projected to dominate the market during the forecast period from 2014 to 2020. Rising number of day surgeries performed in countries such as Denmark, Netherlands, Sweden and other regions will help Rest of Europe to record high number of ambulatory surgeries.

Some of the key players having presence in the Europe Ambulatory Surgical and Emergency Center market are Community Health Systems, Inc., IntegraMed America, Inc., Nueterra Healthcare, Terveystalo Healthcare Oyj, Symbion, Inc., AmSurg Corporation, Medical Facilities Corporation, Surgery Partners, Healthway Medical Corporation Ltd., Eifelhoehen-Klinik AG and others. Among these players, companies such as Community Health Systems, Inc., Healthway Medical Corporation Ltd. and Medical Facilities Corporation have the presence in majority of ambulatory surgeries.

List of Figures

FIG. 1 Europe Ambulatory Surgical Emergency Center Services Market: Market Segmentation

FIG. 2 Europe Ambulatory Surgical and Emergency Center Services Market Revenue, by Types of Procedures, 2013 (USD Million)

FIG. 3 Europe Ambulatory Surgical and Emergency Center Services Market (Volume %), by Types of Procedures, 2013

FIG. 4 Comparative Analysis: Europe Ambulatory Surgical and Emergency Center Services Market, by Country, 2013 and 2020 (Value %)

FIG. 5 Comparative Analysis: Europe Ambulatory Surgical and Emergency Center Services Market, by Country, 2013 and 2020 (Volume %)

FIG. 6 Waiting time from specialist appointment to treatment for Cataract Surgery (2006-2011)

FIG. 7 Porter’s Five Forces Analysis: Europe Ambulatory Surgical & Emergency Center Services Market

FIG. 8 Market Attractiveness Analysis: Europe Ambulatory Surgical & Emergency Center Services Market, by Geography

FIG. 9 Europe Ophthalmology Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 10 Europe Ophthalmology Procedures Market Volume, 2012 - 2020 (No. of Procedures)

FIG. 11 Europe Gastrointestinal Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 12 Europe Gastrointestinal Procedures Market Volume, 2012 - 2020 (No. of Procedures)

FIG. 13 Europe Pain Management Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 14 Europe Pain Management Procedures Market, 2012 - 2020 (No. of Procedures)

FIG. 15 Europe Orthopedics Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 16 Europe Orthopedics Procedures Market Volume, 2012 - 2020 (No. of Procedures)

FIG. 17 Europe Dermatology Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 18 Europe Dermatology Procedures Market Volume, 2012 - 2020 (No. of Procedures)

FIG. 19 Europe ENT Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 20 Europe ENT Procedures Market Volume, 2012 - 2020 (No. of Procedures)

FIG. 21 Europe Urology Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 22 Europe Urology Procedures Market Volume, 2012 - 2020 (No. of Procedures)

FIG. 23 Europe Obstetrics Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 24 Europe Obstetrics Procedures Market Volume, 2012 - 2020 (No. of Procedures)

FIG. 25 Europe Vascular Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 26 Europe Vascular Procedures Market Volume, 2012 - 2020 (No. of Procedures)

FIG. 27 Europe General Surgery Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 28 Europe General Surgery Procedures Market Volume, 2012 - 2020 (No. of Procedures)

FIG. 29 Europe Pulmonary Procedures Market Revenue, 2012 - 2020 (USD Million)

FIG. 30 Europe Pulmonary Procedures Market Volume, 2012 - 2020 (No. of Procedures)

FIG. 31 Heat Map Analysis of Key Market Players of the Ambulatory Surgical & Emergency Center Services Market

FIG. 32 AmSurg Corp.: Annual Revenue, 2011 – 2013 (USD Million)

FIG. 33 Community Health Systems.: Annual Revenue, 2011 – 2013 (USD Million)

FIG. 34 Eifelhöhen Klinik AG: Annual Revenue, 2011 – 2013 (USD Million)

FIG. 35 Healthway Medical Corporation Limited.: Annual Revenue, 2011 – 2013 (USD Thousand)

FIG. 36 Medical Facilities Corporation.: Annual Revenue, 2011 – 2013 (USD Million)

FIG. 37 Symbion, Inc.: Annual Revenue, 2011 – 2013 (USD Million)

Copyright © Transparency Market Research, Inc. All Rights reserved

Trust Online

Ambulatory Surgical & Emergency Center Services Market