Reports

Reports

In the last five years, the global organic dairy market has remained stable. There were a number of reasons behind this which include low shelf premium and strong market penetration especially in yogurt and milk. In addition, brand developments and continuous marketing investment from key market players have contributed to stable sales. Organic dairy industry is also witnessing new markets in developing economies such as China and India. China and India have the advantage of having large organic farmlands, which makes them potential markets for organic dairy industry in the future.

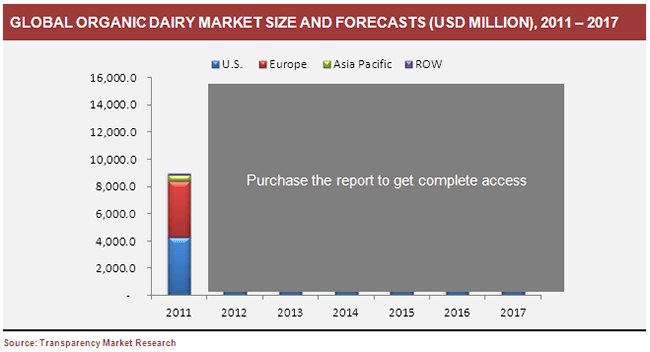

The global organic dairy foods and drinks market was worth USD 9,357.4 million in 2011 and is further expected to grow at a CAGR of 9.1% from 2011 to 2017. In 2011, the organic dairy market was dominated by the U.S. and Europe, which together accounted for 93.1% of the global demand. The U.S. and Europe are estimated to show steady growth rate of 8.2% and 7.9% respectively during 2012.

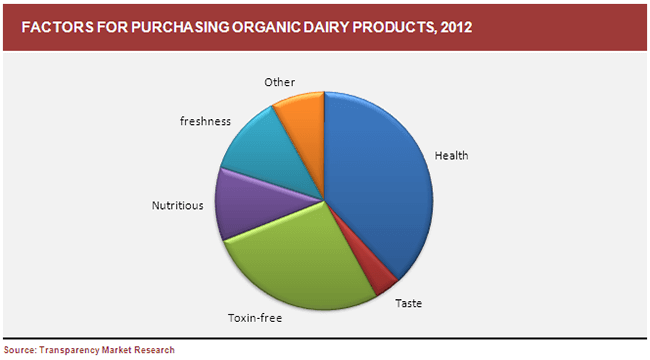

Consumers in the age group from 38 to 45 years are primary consumers of organic dairy products and also are more concerned about food safety and pesticide / chemical residues in food products. As the figure below depicts, consumers purchase organic dairy food and drinks products primarily because of food safety and health concerns. Elderly consumers in the age group of 46 to 65 years give top priority to healthy and safe eating.

1. Introduction

1.1. Report Description

1.2. Methodology

2. Executive Summary

3. Global Organic Dairy Foods & Drinks Market Analysis

3.1. Market Overview

3.2. Organic Dairy Market

3.2.1. Global Organic Dairy Market RevenU.S.By Geography (Usd Million), 2011 Vs 2017

3.2.2. Global Organic Dairy Market Forecast By Geography (Usd Million), 2012-2017

3.2.3. Drivers

3.2.3.1. Consumer’s Preference Shifting From Price Centered To Quality Centered When It Comes To Health

3.2.3.2. Increasing Awareness Of Consumers Towards Organic Dairy Products

3.2.3.3. Government Regulatory Authorities Promoting Organic Products Programs

3.2.3.4. Increasing Demand Of Organic Milk

3.2.3.5. Positive Impact Of Low Interest Rate On Organic Dairy Food And Drink Industry

3.2.3.6. Availability Of Large Variety Of Organic Dairy Products Driving The Organic Dairy Market

3.2.4. Restraints

3.2.4.1. Private Labels And Fake Organic Dairy Products Labels

3.2.4.2. Pricing Of Organic Dairy Product Is Difficult When Dealing With Retailers And Wholesalers

3.2.4.3. Negative Impact Of Lack Of Promotion Of Dairy Products

3.2.4.4. Higher Input Cost Involved In Organic Milk Production Will Remain A Constraint

3.2.4.5. Ongoing Research And Development Cost

3.3. Regulation

3.3.1. Europe

3.3.2. U.S.

4. Pricing Analysis And Market Forecast

4.1. Overview

4.1.1. Typical Organic Milk Price Premi U.S.

4.2. U.S.

4.2.1. Average Price Of Organic Milk In The U.S., 2008-2017

4.2.2. Price Gap Between Organic And Non-organic Milk In The U.S., 2008-2017

4.2.3. U.S. Organic Dairy Market

4.2.3.1. U.S. Organic Dairy Products Market Size And Forecast

4.2.3.2. U.S. Organic Milk Market Size And Forecast, 2011-2017

4.2.3.3. U.S. Yogurt Market Size And Forecast, 2011-2017

4.2.3.4. U.S. Cheese Market Size And Forecast, 2011-2017

4.2.3.5. U.S. Other Dairy Product Market Size And Forecast, 2011-2017

4.3. Europe

4.3.1. Historical Average Price Of Organic Milk In Europe (Euro/100kg), 2005-2011

4.3.2. Forecasted Average Price Of Organic Milk In Europe (Euro/100kg), 2012-2017

4.3.3. Historical Average Price Of Non-organic Milk In Europe (Euro/100kg), 2005-2011

4.3.4. Forecasted Average Price Of Non-organic Milk In Europe (Euro/100kg), 2012-2017

4.3.5. European Organic Dairy Market

4.3.5.1. European Organic Dairy Products Market Size And Forecast (Usd Million), 2011-2017

4.3.5.2. European Organic Milk Market Size And Forecast (Usd Million), 2011-2017

4.3.5.3. European Yogurt Market Size And Forecast (Usd Million), 2011-2017

4.3.5.4. European Cheese Market Size And Forecast (Usd Million), 2011-2017

4.3.5.5. European Other Dairy Product Market Size And Forecast (Usd Million), 2011-2017

4.4. Asia Pacific

4.4.1. Average Price Of Organic Milk In Asia Pacific, 2008-2017

4.4.2. Average Price Of Non-organic Milk (Usd/half Gallon) In Asia Pacific, 2008-2017

4.4.3. Asia Pacific Organic Dairy Market

4.4.3.1. Asia Pacific Organic Dairy Products Market Size And Forecast (Usd Million), 2011-2017

4.4.3.2. Asia Pacific Organic Milk Market Size And Forecast, 2011-2017

4.4.3.3. Asia Pacific Yogurt Market Size And Forecast, 2011-2017

4.4.3.4. Asia Pacific Cheese Market Size And Forecast, 2011-2017

4.4.3.5. Asia Pacific Other Dairy Product Market Size And Forecast, 2011-2017

4.4.4. Row Organic Dairy Market

4.4.4.1. Row Organic Dairy Products Market Size And Forecast (Usd Million), 2011-2017

5. Korea Organic Dairy Market Analysis

5.1. Overview

5.1.1. Korean Consumer Behavior For Organic Product

5.2. Reasons To Purchase Organic Products In South Korea

5.3. Barriers To Purchase Organic Products In South Korea

5.4. Major Korean Organic Dairy Companies And Their Products In Market

5.5. Raw Milk (Regular) Supply & Demand Prospects From 2007. To 2021 (1,000 Metric Ton)

5.6. Per Capita Milk (Kilo Gram) Consumption Trend In South Korea, 2007-2021

5.7. Korean Labeling System

5.8. Market Strategy

5.8.1. Promotional Activities

5.8.1.1. Organic & Natural Trade Fair 2012

5.8.1.2. Seoul Food & Hotel 2013. (Goyang, Korea)

5.8.1.3. Samyang Corporation (Guten Morgen Organic Retailer)

5.8.1.4. Business Strategy

5.9. Porter’s Five Force Analysis

5.9.1. Bargaining Power Of Supplier

5.9.2. Bargaining Power Of Buyer

5.9.3. Rivalry Among Existing Competitors (Moderate)

5.9.4. Threat Of New Entrants

5.9.5. Threat Of SU.S.itute Products

5.10. Market Drivers

5.10.1. Increasing Awareness Of Korean Consumers Towards Organic Dairy Products

5.10.2. Rise In Imported Organic Dairy Products Implies More Demand In Domestic Market

5.10.3. Educated Consumers Driving The Korean Organic Dairy Market

5.10.4. Increasing Government Support

5.11. Restraints

5.11.1. Rise In Interest Rates In Korea Will Restrain The Market Growth

5.11.2. Lack Of Pasture In Korea Will Restrain The Growth Of Organic Dairy Farms

5.11.3. Premium Price Will Restrain The Market Growth

5.12. Price Analysis

5.12.1. Average Price Of Organic Milk In Asia Pacific, 2008-2017

5.12.2. Average Price Of Non-organic Milk (Usd/half Gallon) In South Korea, 2008-2017

5.13. South Korea Organic Dairy Market

5.13.1. South Korea Organic Dairy Products Market Size And Forecast (Usd Million), 2011-2017

5.13.2. South Korea Organic Milk Market Size And Forecast, 2011-2017

5.13.3. South Korea Yogurt Market Size And Forecast, 2011-2017

5.13.4. South Korea Cheese Market Size And Forecast, 2011-2017

5.13.5. South Korea Other Dairy Product Market Size And Forecast, 2011-2017

List Of Figures

Fig. 1: Global Organic Foods Market RevenU.S.By Product Type, 2011

Fig. 2: Global Organic Dairy Market Size By Geography (USD Million), 2011 Vs 2017

Fig. 3: Global Organic Dairy Market Forecast By Geography (USD Million), 2012-2017

Fig. 4: Estimated Total U.S. Sales Of Organic Fat-reduced Milk For First Three Months In USD Million (2009-2012)

Fig. 5: Average Price Of Organic Milk In The U.S. (USD/half Gallon), 2008-2017

Fig. 6: Price Gap Between Organic And Non-organic Milk Retail Pricing In The U.S. (USD/half Gallon), 2008-2017

Fig. 7: U.S. Organic Dairy Products Market Size And Forecast (USD Million), 2011-2017

Fig. 8: U.S. Organic Milk Market Size And Forecast (USD Million), 2011-2017 30

Fig. 9: U.S. Yogurt Market Size And Forecast (USD Million), 2011-2017

Fig. 10: U.S. Cheese Market Size And Forecast (USD Million), 2011-2017

Fig. 11: U.S. Other Dairy Product Market Size And Forecast (USD Million), 2011-2017

Fig. 12: Historical Average Price Of Organic Milk In Europe (Euro/100kg), 2005-2011

Fig. 13: Forecasted Average Price Of Organic Milk In Europe (Euro/100kg), 2012-2017

Fig. 14: Historical Average Price Of Non-organic Milk In Europe (Euro/100kg), 2005-2011

Fig. 15: Forecasted Average Price Of Non-organic Milk In Europe (Euro/100kg), 2012-2017

Fig. 16: European Organic Dairy Products Market Size And Forecast (USD Million), 2011-2017

Fig. 17: European Organic Milk Market Size And Forecast (USD Million), 2011-2017

Fig. 18: European Yogurt Market Size And Forecast (USD Million), 2011-2017 36

Fig. 19: European Cheese Market Size And Forecast (USD Million), 2011-2017 37

Fig. 20: European Other Dairy Product Market Size And Forecast (USD Million), 2011-2017

Fig. 21: Average Price Of Organic Milk In Asia Pacific (USD/half Gallon), 2008-2017

Fig. 22: Average Price Of Non-organic Milk (USD/half Gallon) In Asia Pacific (USD/half Gallon), 2008-2017

Fig. 23: Asia Pacific Organic Dairy Products Market Size And Forecast (USD Million), 2011-2017

Fig. 24: Asia Pacific Organic Milk Market Size And Forecast (USD Million), 2011-2017

Fig. 25: Asia Pacific Yogurt Market Size And Forecast (USD Million), 2011-2017

Fig. 26: Asia Pacific Cheese Market Size And Forecast (USD Million), 2011-2017 42

Fig. 27: Asia Pacific Other Dairy Product Market Size And Forecast (USD Million), 2011-2017

Fig. 28: Row Organic Dairy Products Market Size And Forecast (USD Million), 2011-2017

Fig. 29: Reasons To Purchase Organic Products In South Korea

Fig. 30: Barriers To Purchase Organic Products In South Korea

Fig. 31: Purchase Channel For Organic Products In South Korea

Fig. 32: Per Capita Consumption Of Milk (Kilo Gram) In South Korea

Fig. 33: Organic Labeling In South Korea

Fig. 34: Porter’s Five Force Analysis

Fig. 35: Average Price Of Organic Milk In South Korea (USD/half Gallon), 2008-2017

Fig. 36: Average Price Of Non-organic Milk (USD/half Gallon) In South Korea (USD/half Gallon), 2008-2017

Fig. 37: South Korea Organic Dairy Products Market Size And Forecast (USD Million), 2011-2017

Fig. 38: South Korea Organic Milk Market Size And Forecast (USD Million), 2011-2017

Fig. 39: South Korea Yogurt Market Size And Forecast (USD Million), 2011-2017

Fig. 40: South Korea Cheese Market Size And Forecast (USD Million), 2011-2017

Fig. 41: South Korea Other Dairy Product Market Size And Forecast (USD Million), 2011-2017

Copyright © Transparency Market Research, Inc. All Rights reserved

Trust Online

Organic Dairy Products (Foods And Drinks) Market